There is a continuing trend towards people having a longer and more active retirement, and a need for retirees to be able to finance more of their retirement lifestyle themselves.

Retirement planning involves not only saving for your retirement but structuring your affairs to maximise your government benefits and after-tax incomes. Later in retirement you may also need to consider aged care accommodation.

Retirement planning involves not only saving for your retirement but structuring your affairs to maximise your government benefits and after-tax incomes. Later in retirement you may also need to consider aged care accommodation.

For most people, one of the major financial planning objectives is to ensure they have saved enough during their working life to be able to afford a comfortable retirement lifestyle.

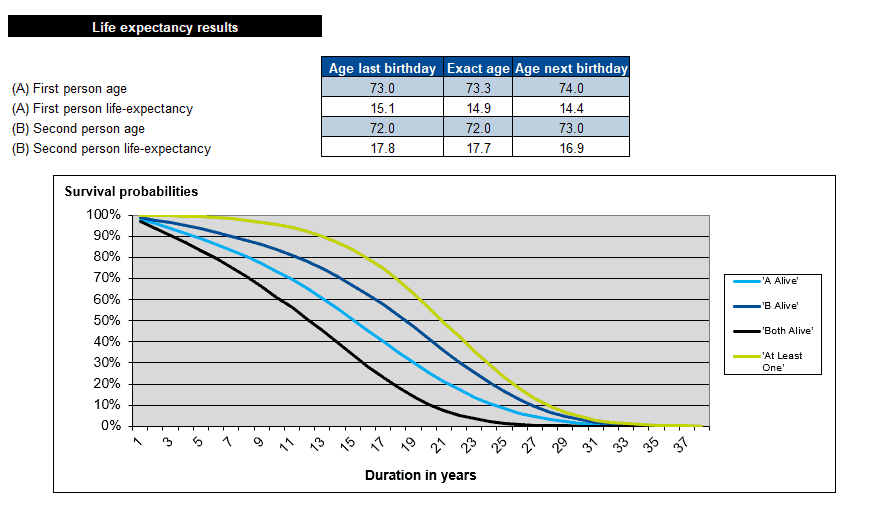

With advances in medical science and a trend towards earlier retirement, the period the average Australian spends in retirement is getting longer. Your retirement plans should not be based on using up your capital based on your life expectancy – there is a 50% chance you will run out of money well before you die.

People are also seeking a more active and fulfilling retirement, requiring larger sums of capital to fund the desired lifestyle.

Effective retirement savings strategies could involve combinations of accelerated debt repayments, voluntary superannuation contributions, investment properties and a regular investment program.

There are a number of ways to structure your investments during your retirement. How the investments are structured will have implications in respect of:

- Social security pension eligibility;

- Taxation; and

- Longevity risk (i.e. the risk your funds run out).

Have you thought about what do you want to do in retirement, and what it will cost?

How much retirement capital will you need?

Aged Pensions

The age pension is provided by the Government through Centrelink as a safety-net provision for people who need help meeting their income needs in retirement. Effective planning can help you maximise your entitlements and preserve your own capital.

Have you thought about what do you want to do in retirement, and what it will cost?

How much retirement capital will you need?

Estate Planning

As part of the financial planning process we discuss your options and assist you to clarify your wishes. We then provide you with recommendations as to how you can ensure these wishes are complied with in a manner that is financially efficient and tax-effective, reducing the burden on the loved ones you leave behind.

Further information on Estate Planning

Aged Care Needs

After a lifetime of independent living, it is hard to admit that you may need help with some of the daily activities of life.

Planning early and seeking professional advice will help to ensure you receive the best level of care you can afford.

Different people need help with different things— some will need help for mobility reasons, others may need help with meals and household chores.

Different people need help with different things— some will need help for mobility reasons, others may need help with meals and household chores.

There are a number of government funded in-home care service programs (some fees may apply) that may meet their needs, allowing them to remain in their own home for longer.

At some stage a person may no longer be able to look after themselves at home. Sometimes the person will may realize they have reached this stage themselves, but often it is their children that will make the decision.

For some families the right decision will be for the person to move in with a family member, for other families it may be more appropriate that the care is provided in a professional aged care facility.

Accommodation Alternatives

The main types of aged care accommodation facilities are:

- Retirement villages

Predominantly self-care with external building and garden maintenance undertaken by the village operator. Assistance with meals may be available upon request. - Hostels

Low level care facility. - Nursing homes

High level care facility.

Prior to entry to a hostel or nursing home, assessment of the level of care needed is undertaken by an ACAT team (including social workers, doctors and other health professionals).

Planning Early Provides the Best Opportunities

After a lifetime of independent living, it is hard to admit that you may need help with some of the daily activities of life.

Planning early and seeking professional advice will help to ensure you receive the best level of care you can afford.

While the ongoing fees charged by hostels and nursing homes are regulated by government, how your financial affairs are structured can have a big impact on:

- The amount of aged care fees you have to pay;

- The amount of any age pension you may be entitled to receive; and

- Whether or not you can afford to keep the family home.

Financial Guidance

Broadening the scope of the financial planning mandate to include your wider family group can open a number of additional planning opportunities to benefit your whole family.

The biggest priority for most people is making sure their family is well cared for. We do this in several ways, including teaching our children the difference between right and wrong, ensuring they have the appropriate medical treatment, and giving them the best education we can afford.

From a financial perspective, one of the best things we can do for our children is ensure they understand money—how hard it is to make, how easy it is to lose, and the things it can allow them to do with their lives.

A basic understanding of money and finance concepts will not only help them with their day to day lives, but it will mean they are more likely to seek and benefit from professional financial advice for the major decisions.

A Helping Hand

At some stage in our lives we all want to give a family member a helping hand financially. Some of the more common reasons are to help with a deposit on their first home, pay for their wedding, or to help pay for the costs of a better education. As experienced financial advisors, we can help you plan your affairs to be able to provide this helping hand.

Mitigating Risks

Often an unexpected illness or accident may leave a child with a permanent disability and the need for ongoing care. Apart from the emotional distress, the financial costs and possible reduction in the parent’s employment income can have a significant impact on you achieving your financial goals. This risk can generally be mitigated or transferred to an insurance company.

Families Working Together

Families can often achieve better financial outcomes and improved lifestyles if they work together. Examples of family focused strategies that can benefit more than one generation include;

- Use of family self-managed superannuation funds to increase the investment opportunities for the members, or transfer wealth between generations tax-effectively;

- Granny flat accommodation for elderly parents;

- Business succession planning;

- Providing collateral security or a guarantee to help your children buy their first home.